The new analysis for Carbon Brief, based on official figures and commercial data, shows rapid electricity demand growth and weak rains boosted demand for coal power in 2023, while the rebound from zero-Covid boosted demand for oil.

Other key findings from the analysis include:

- China’s CO2 emissions have now increased by 12 per cent between 2020 and 2023, after a highly energy- and carbon-intensive response to the Covid-19 pandemic.

- This means CO2 emissions would need to fall by 4-6 per cent by 2025, in order to meet the target of cutting China’s carbon intensity – its CO2 emissions per unit of economic output – by 18 per cent during the 14th five-year plan period.

- China is also at risk of missing all of its other key climate targets for 2025, including pledges to “strictly limit” coal demand growth and “strictly control” new coal power capacity, as well as targets for energy intensity, the share of low-carbon energy in overall demand and the share of renewables in energy demand growth.

- Government pressure to hit the targets, most of which are in China’s updated international climate pledge under the Paris Agreement, makes it more likely that China’s CO2 emissions will peak before 2025 – far earlier than its target of peaking “before 2030”.

The deadline for peaking CO2 emissions has led officials and industries to pursue rapid emissions growth and carbon-intensive projects, while a window to do so remains open.

The government recently recognised and responded to the gap to meeting its targets, by calling for stronger controls on such projects, as well as faster renewables deployment.

Most of China’s climate targets can be met if the acceleration of clean energy deployment during 2023 is maintained – and if energy demand growth returns to pre-Covid levels.

China’s CO2 emissions continued to increase in 2023

According to preliminary official data, China’s total energy consumption increased by 5.7 per cent in 2023, the first time since at least 2005 that energy demand has grown faster than GDP.

With coal consumption growing by 4.4 per cent, our analysis shows CO2 emissions increasing by 5.2 per cent – at the same rate as GDP – highlighting energy-intensive recent growth patterns.

China’s economic growth during and after the Covid-19 pandemic has been highly energy- and carbon-intensive. CO2 emissions grew at an average of 3.8 per cent per year in 2021-23, up from 0.9 per cent a year in 2016-20, while GDP growth slowed from an average of 5.7 per cent to 5.4 per cent.

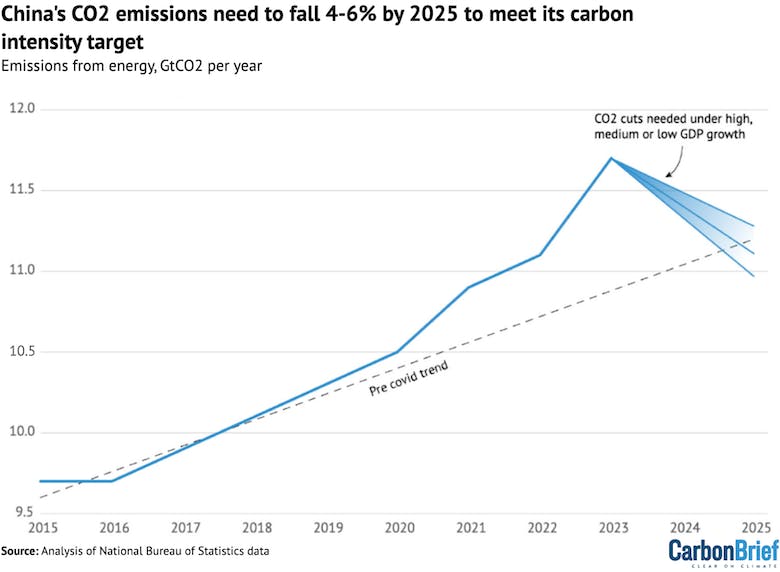

Another year of rapidly rising emissions in 2023 leaves China way off track against its target of cutting carbon intensity by 18 per cent during the 14th five-year plan (2021-25).

As a result, CO2 emissions would now need to fall by 4-6 per cent by 2025 to hit the goal. This is illustrated in the figure below, showing historical emissions (black line) and the reductions needed by 2025 to hit the carbon intensity target, depending on the rate of GDP growth.

Even if China’s GDP growth is high and averages 6 per cent per year in 2024-25, the intensity target requires CO2 emissions to fall by 4 per cent.

China’s CO2 emissions from energy, billion tonnes per year, and the reductions needed by 2025 to hit the carbon intensity target under low (4.5 per cent), medium (5.2 per cent) or high (6.0 per cent) rates of GDP growth in 2024-25. Note the truncated y-axis. Source: Author calculations using official national bureau of statistics data. Chart by Carbon Brief.

The main drivers of the emissions increase in 2023 were coal-fired power and oil consumption, which increased by 6 per cent and 8 per cent, respectively.

A major reason for the growth in power generation from coal was that hydropower operating rates reached the lowest level in more than two decades due to a series of droughts. These operating rates are likely to recover towards average levels in 2024.

The increase in oil consumption represents a rebound from the slow demand growth during zero-Covid and an outright drop in 2022. Gas consumption rebounded as prices came down from 2022 highs, while still remaining elevated.

The clean energy manufacturing boom also has a role in driving emissions, due to energy-intensive processes involved in the production of solar PV and batteries, in particular.

Approximately one percentage-point of CO2 emission growth can be attributed to these sectors, based on output data and emission intensities estimated for solar PV, electric vehicles and batteries.

This means that, without the clean technology manufacturing boom, China’s CO2 emissions would have grown by around 4.2 per cent, instead of the 5.2 per cent estimated in our analysis.

Nevertheless, the increase in manufacturing will result in a significant reduction in emissions in net terms, once the products are in use. About half of this reduction will be realised outside of China, as the products are exported.

China is off track to all of its 2025 climate targets

China’s climate pledge under the Paris Agreement (nationally determined contribution, NDC) was updated in 2021, following commitments made by President Xi Jinping earlier that year and incorporating targets set under the 14th five-year plan.

The updated NDC makes commitments to strictly limit coal consumption growth; strictly control new coal power; reduce energy and carbon intensity by 2025; and increase the share of non-fossil energy sources to 25 per cent by 2030.

In addition, the country’s five-year plans set targets of increasing the share of non-fossil energy sources to 20 per cent by 2025 and deriving more than 50 per cent of the increase in energy use from 2020 to 2025 overall from renewable sources.

All of these targets are severely off track after 2023.

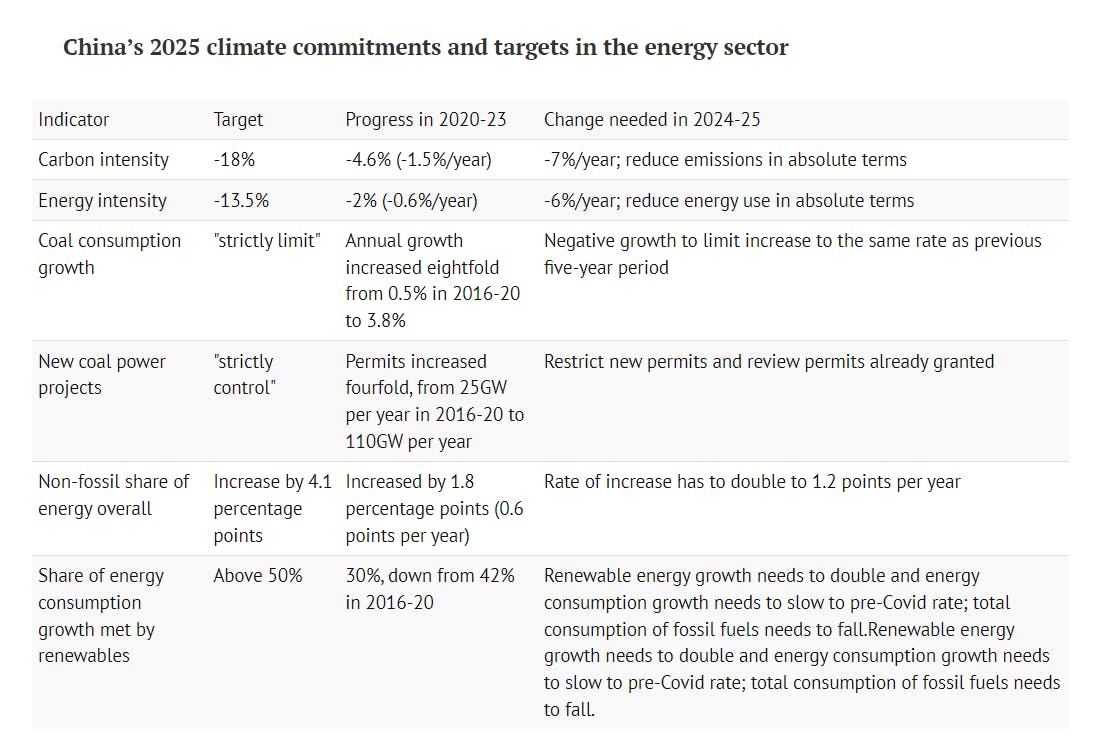

The table below lists the various climate- and energy-related targets, the progress seen from 2020-23 and what would be needed during 2024-25 to achieve each of the goals. (See below for further details on each indicator and what is needed by 2025.)

Chart by Carbon Brief.

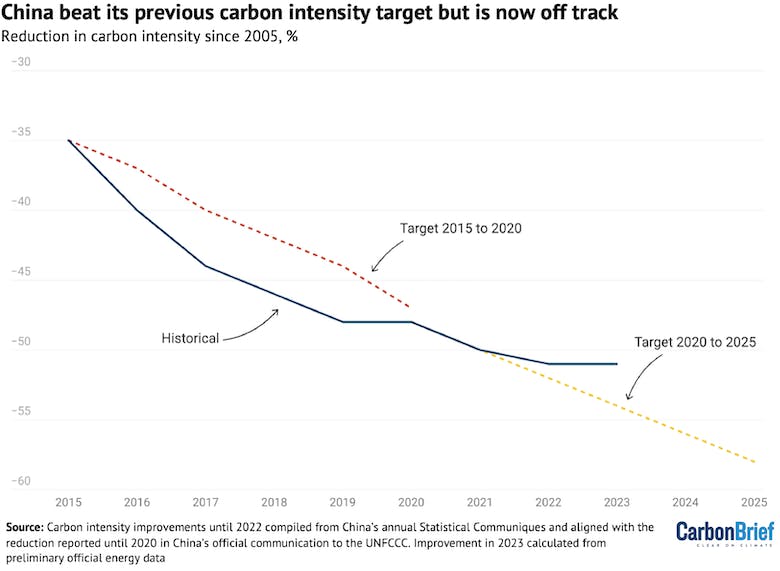

The centrepiece of China’s 2020 and 2025 climate commitments has been reducing carbon intensity, or CO2 emissions from energy use per unit of GDP.

The country’s carbon intensity reportedly fell 48 per cent from 2005 to 2020. China committed to an 18 per cent fall from 2020 to 2025 – and to reducing carbon intensity by more than 65 per cent from 2005 levels by 2030, which requires a further reduction of at least 17 per cent from 2025 to 2030.

However, as of the end of 2023, China’s carbon intensity has only fallen 5 per cent in the 14th five-year plan period, lagging far behind the target of 18 per cent from 2020 to 2025. If this target is to be met, CO2 emissions will have to come down in absolute terms from 2023 to 2025.

The figure below shows how China overachieved against its carbon intensity target for 2015-2020 but is veering increasingly off track against the goal for 2020-2025.

Change in carbon intensity since 2005, per cent, and targets under the 13th and 14th five year plans. Source: Carbon intensity improvements until 2022 compiled from China’s annual Statistical Communiques and aligned with the reduction reported until 2020 in China’s official communication to the UNFCCC. Improvement in 2023 calculated from preliminary official energy data. Chart by Carbon Brief.

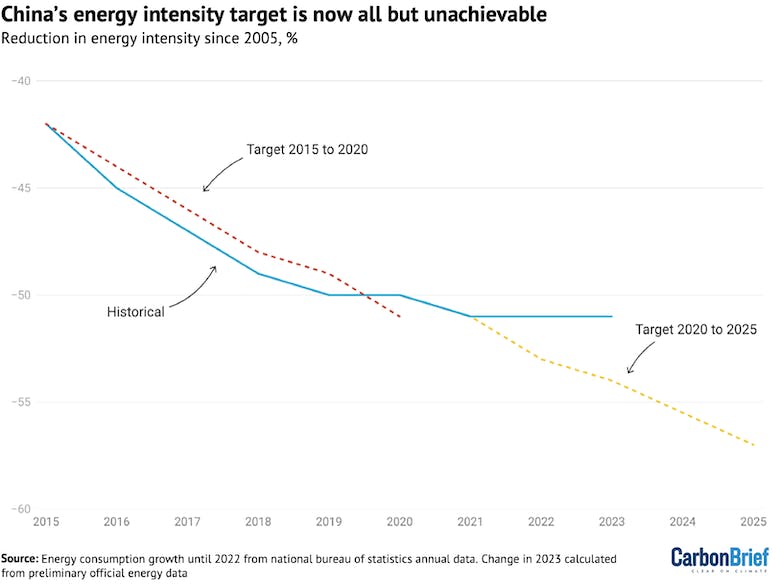

China’s energy intensity increased by 0.5 per cent in 2023, the first annual rise since at least 2005. From 2020 to 2023, energy intensity only fell 2 per cent.

The figure below shows that China narrowly missed its energy intensity target during the 13th five-year plan period, spanning 2016 to 2020, as progress halted in 2020. The country is now far off track for its 14th five-year plan target.

Indeed, to meet the target of a 13.5 per cent reduction over 2020-25 – given the lack of progress as of the end of 2023 – energy consumption would have to fall in absolute terms over the next two years, while the rate of GDP growth is maintained or accelerated. This makes the goal all but unachievable.

Change in energy intensity since 2005, per cent, and targets under the 13th and 14th five year plans. Source: Energy consumption growth until 2022 from national bureau of statistics annual data. Change in 2023 calculated from preliminary official energy data. Chart by Carbon Brief.

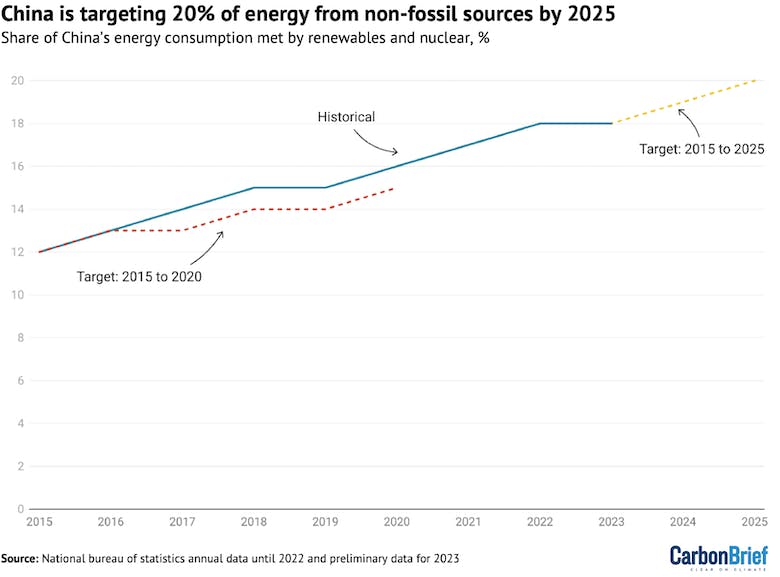

The share of China’s energy demand met by non-fossil sources has increased by 1.8 percentage points from 2020 to 2023, against a target of 4.1 points by 2025.

This is shown in the figure below, illustrating the targeted 15 per cent share for non-fossil energy by 2020 and 20 per cent by 2025, as well as progress to date.

Meeting the 2025 target would mean that the rate of increase needs to double for the next two years. Moreover, if energy demand growth continues at the exceptionally high rate of 2020 to 2023, then energy production from non-fossil sources would need to grow at 11.3 per cent per year to meet the target, up from 8.5 per cent in the past three years.

Alternatively, the growth of renewables and nuclear could be maintained – but energy consumption growth would have to slow down to its pre-Covid average.

Share of energy consumption met by non-fossil sources, per cent, and targets under the 13th and 14th five year plans. Source: National bureau of statistics annual data until 2022 and preliminary data for 2023. Chart by Carbon Brief.

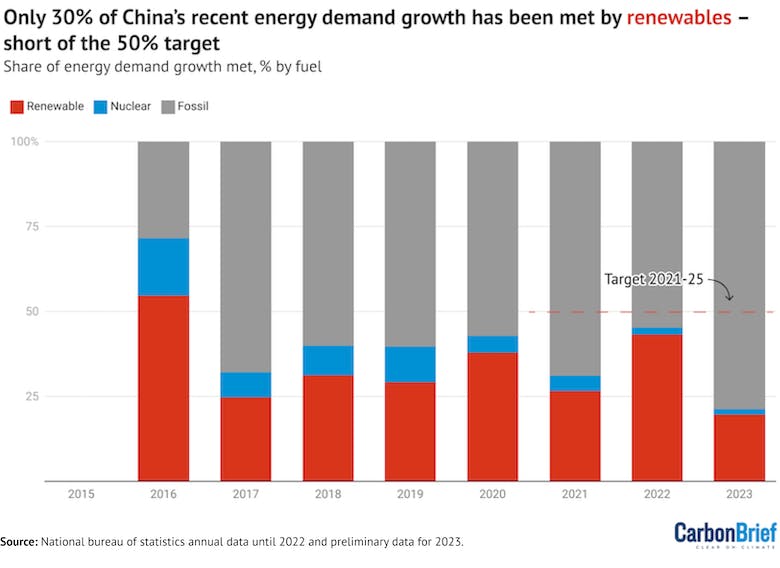

Only 30 per cent of energy consumption growth has been met by renewable energy in 2020 to 2023, against a target of more than 50 per cent during 2020-25.

This is illustrated in the figure below, showing contributions to annual energy demand growth from fossil fuels (grey bars), nuclear (blue) and renewables (red).

The 50 per cent target is now highly unlikely to be met without a slowdown in energy consumption growth. Without a slowdown, renewables would have to grow by 20 per cent per year to meet the target, up from 8.9 per cent in the past three years.

Share of energy demand growth met by fossil fuels (grey), nuclear (blue) and renewables (red), per cent, and the target for 2020-2025 (red dashed line). Source: National bureau of statistics annual data until 2022 and preliminary data for 2023. As the headline energy supply statistics only report the total for nuclear and renewables, the contribution of nuclear is disaggregated using electricity generation data in national bureau of statistics industrial output statistics. Chart by Carbon Brief.

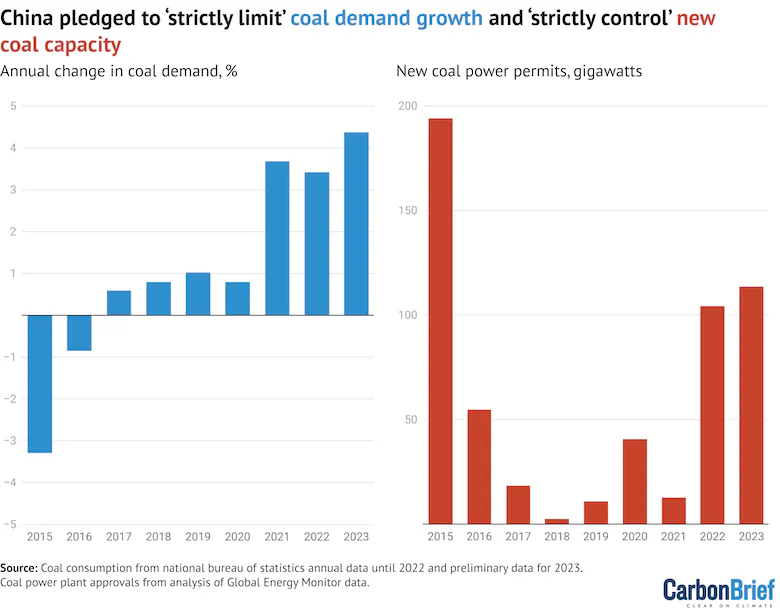

Both growth in coal consumption and new coal power projects accelerated sharply in 2021-23, despite Xi’s pledges to “strictly control” them.

This is illustrated in the figure below, with annual coal consumption growth on the left and the amount of new coal capacity added each year on the right.

Indeed, the average growth rate of coal consumption increased 8-fold from 0.5 per cent per year in 2016-20 to 3.8 per cent per year in 2021-23.

Similarly, new coal power approvals increased fourfold in 2022-23, compared with the five years before the “strictly control” pledge, based on analysis of Global Energy Monitor data.

Left: Coal consumption growth per year, per cent. Right: Capacity of new coal power plants given permits, gigawatts. Source: Coal consumption from national bureau of statistics annual data until 2022 and preliminary data for 2023. Coal power plant approvals from analysis of Global Energy Monitor data. Charts by Carbon Brief.

Since the beginning of 2022, a total of 218 gigawatts (GW) of new coal power plants have been permitted. By the end of 2023, some 89GW of this capacity had already started construction, while 128GW had yet to break ground.

Furthermore, the government’s official policy has shifted to strongly encouraging new coal power. An assessment of the projects permitted in 2022-23 shows that requirements, set for approving new coal power plants in August 2021, have not been enforced.

Statements from developers and government officials – see below – confirm that the 14th five-year plan period until 2025 is being seen as a “window of opportunity” for new coal power plants, rather than a period when new projects are strictly controlled.

This is causing a rush to secure permits for new projects. China Shenhua called the period until 2025 “an opportune time for thermal power construction”. The provincial state-owned enterprise supervisor boasts of Inner Mongolia Energy Group “achieving a flying start” to 2023 and “seizing the policy window” for coal power projects.

The Zhejiang province energy regulator emphasised the importance of seizing the time window for thermal power construction during the 14th five-year period.

Power China called for joint efforts with local government officials to exploit the coal power development window effectively, citing a plan known as “three times 80GW”. This refers to a proposal promoted by the thermal power construction industry to permit and commission 80GW of coal power plants each year, from 2022 to 2024.

The meaning of the pledges to “strictly control” growth in coal consumption and new coal power projects lacks a precise definition. However, a sharp acceleration of coal consumption growth and coal power plant approvals, along with active government promotion of new projects, is hard to reconcile with the pledge to exert strict control.

By this logic, meeting the pledge on coal consumption growth would require, at the very least, reducing coal use from 2023 to 2025 to bring the growth rate during the 2021 to 2025 period closer to the rate during the preceding five-year period.

Similarly, meeting the commitment to control new coal power projects would require enforcing existing policy to limit new schemes, restricting new permits and reviewing permits already granted, to limit the acceleration compared with the preceding five-year period.

Official energy data is over-reporting coal consumption growth

In 2022, government policies seeking to increase coal mine output and push down coal prices led to a sharp deterioration in the quality and calorific value of coal produced.

This fall in quality meant that the weight of coal being consumed increased by far more than the amount of energy supplied or CO2 emitted from that coal.

China’s official statistics failed to capture the change and consequently over-reported the growth in coal consumption and under-reported the improvement in CO2 intensity in 2022. This 2022 data could be expected to be revised once more complete energy statistics are released later.

Unlike in 2022, the officially-reported coal consumption growth rate for 2023 is more closely aligned with growth in coal power generation and output in key heavy industry sectors. The data indicates that coal use grew 4.4 per cent in 2023, while power generation from coal rose 6 per cent.

However, the conclusion that CO2 emissions need to fall from 2023 to 2025 to meet the carbon intensity target holds, even if a correction to 2022 data is made.

Calculating with current official data, CO2 emissions need to fall by 3.8-6.5 per cent in the next two years, depending on the growth rate of GDP.

Based on my previous estimate that the growth in CO2 emissions in 2022 was inflated by 2.3 percentage points, a correction for 2022 would put the required reduction at 1.6-4.3 per cent.

Government response

Energy intensity and carbon intensity reduction are among the 20 “main indicators” specified in China’s overarching five-year plan for 2021-25.

The mid-term evaluation of progress, published by China’s top economic planner the national development and reform commission (NDRC) in December 2023, identified these indicators as two of the four that were off track, along with a key air quality target.

(Air pollution concentrations also rose in 2023 due to increased industrial and transportation emissions, along with unfavourable weather conditions.)

In late 2023, the NDRC reprimanded the provinces of Hubei, Shaanxi, Gansu, Qinghai, Zhejiang, Anhui, Guangdong and Chongqing for lagging behind on the targets to control energy intensity and total energy consumption.

Zhou Dadi, a member of the national climate change expert advisory committee, pointed to the weak growth in service industries as the reason for the lack of progress on the intensity targets.

Service sectors have relatively low energy demand and carbon emissions relative to economic output, so the decline in their share of economic activity tends to increase the energy and carbon intensity of the economy.

The NDRC’s evaluation report also identified measures to achieve the targets, including improving policies to control energy use and carbon emissions, curbing the initiation of projects with high energy consumption and high emissions, strictly limiting total coal consumption, promoting a shift to cleaner industry and transportation, promoting energy conservation and, importantly, accelerating the deployment of renewable energy.

The clean energy boom can allow most targets to be met

While China fell severely behind on its 2025 climate targets for the energy sector, the past two years saw a veritable boom in clean energy installations – particularly solar power.

This boom puts most of the targets still in reach, especially if energy demand growth returns to the pre-Covid rates.

My earlier analysis showed that China’s CO2 emissions could fall this year and then stabilise, if additions of low-carbon power generation continue at 2023 rates and electricity demand returns to trend.

Under this projection, CO2 emissions fall by approximately 1.5 per cent from 2023 to 2025. Therefore, achieving the 4-6 per cent reduction in CO2 emissions needed to meet the CO2 intensity target from 2023 to 2025 would require further acceleration in clean energy deployment, or a sharp slowdown in energy demand growth.

The increase in the share of non-fossil energy should be possible to achieve given the sharp increase in solar and wind installations in 2023. To start with, slow progress was partially caused by the record-low hydropower operating rates in 2023, linked to record droughts.

Even if energy demand continued to grow at the 2020-23 rate, continued low-carbon energy additions at the 2023 level should suffice to raise the share of non-fossil energy to 21 per cent, comfortably ahead of the target.

The target of renewable energy contributing half of the growth in total energy demand is significantly more challenging.

If energy consumption growth rate slows down to its pre-Covid average and clean energy capacity additions continue at the 2023 rate, enabling the growth rate of renewable energy production to almost double to 16 per cent, then the target would likely be reached.

This would also mean a reduction in the total consumption of fossil fuels and a reduction in energy sector CO2 emissions. This scenario would arguably also meet the commitment to “strictly limit the growth in coal consumption”.

Meeting the pledge to “strictly control” new coal power projects would mean thoroughly assessing the justification for permits granted in the past two years and restricting the issuance of new permits.

The large amount of electricity storage being deployed – especially pumped hydro, but increasingly also grid-connected batteries – reduces the need for thermal power plants.

For a significant restriction of new coal power to be possible while ensuring electricity supply security, progress would also be needed on power system reforms that increase flexibility and make more efficient use of existing capacity.

China’s clean energy boom has been happening much faster than official targets for wind and solar installations would require, driven by enthusiasm from local governments, state-owned enterprises and investors.

However, due to the rapid increase in energy consumption, meeting China’s headline climate targets now requires that the momentum of clean energy installations is maintained.

About the data

Total energy consumption and energy mix were taken from national bureau of statistics annual data. Improvements in energy intensity and carbon intensity were compiled from the bureau’s annual statistical communiques and changes in carbon emissions were calculated based on reported GDP growth and carbon intensity improvement.

Growth in total energy consumption and changes in the energy mix were taken from preliminary information released by the national bureau of statistics. Growth in CO2 emissions in 2023 was calculated using Intergovernmental Panel on Climate Change default emission factors based on changes in the consumption of coal, oil and gas.

This story was published with permission from Carbon Brief.