Governments and utility operators across Asia are challenged with balancing pressures to decarbonise while continuing to meet growing electricity demand with affordable power. While coal remains the dominant source of power generation for many nations in the region today, it is a major source of carbon emissions.

As governments’ efforts to tackle climate change accelerate, asset owners with significant long-term capital tied up in coal-fired generation will need to reconsider the role of their facilities to avoid their assets becoming stranded. Owners must begin planning now for retirement, repurposing with affordable and alternative generation, or further diversification of their business portfolios.

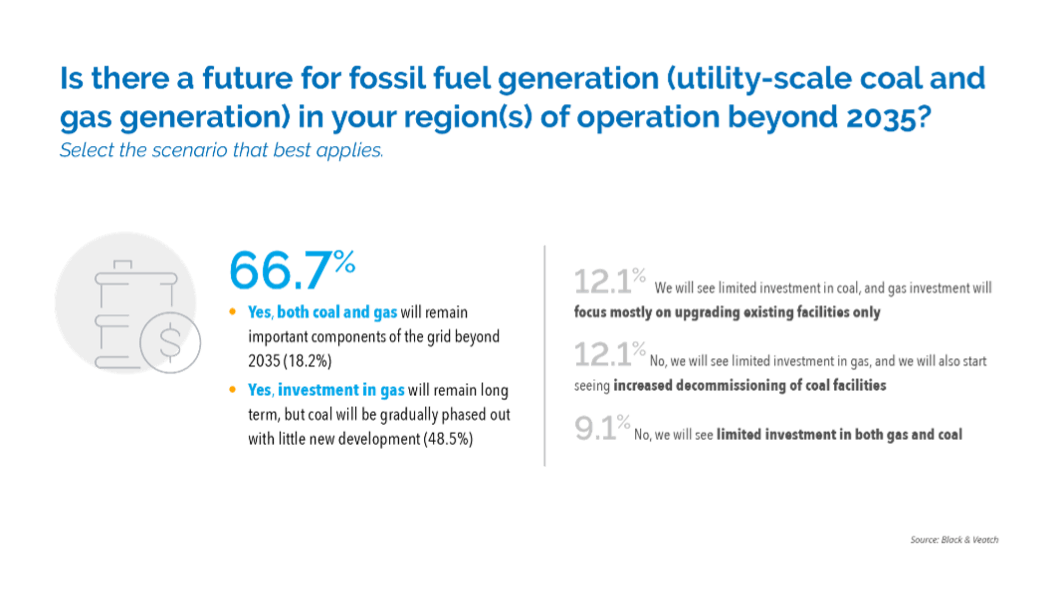

According to Black & Veatch’s Strategic Directions: Electric Industry Asia 2021 report, only 18 per cent of respondents see a future for coal-fired power generation beyond 2035.

Only 18 per cent of respondents see a future for coal-fired power generation beyond 2035. Image: Black and Veatch

In Asia, many governments are already advancing plans and we can expect more announcements and initiatives to follow. For example, the Philippines is planning to acquire and repurpose Mindanao’s coal plants to increase the region’s renewable energy and shift most of its energy requirements to hydropower.

Financial institutions and insurers are also leading the decarbonisation charge. Based on media reports, financial institutions such as the Asian Development Bank, HSBC and Citi, asset managers like BlackRock and insurers such as Prudential are studying a plan to accelerate the retirement of Asia’s coal-fired power plants.

Asset owners are facing mounting pressures from governments, lenders and the public to adopt sustainable means of power generation and conserve resources. Coal-fired plants in Asia will be required to comply with tightening emissions and effluent norms imposed by governments, all impacting profitability.

Price parity achieved by renewables is also resulting in the steady displacement of coal power generation from the grid. This increased contribution of variable renewable generation, along with inadequate ancillary support like energy storage, has also increased cycling of large-scale coal and gas power plants, which in turn, results in additional cost implications.

Against this background, asset owners considering the long-term economic viability of their facilities have several options:

- Full or partial fuel conversion to fuel sources like natural gas, biomass or hydrogen

- Retrofitting emissions control equipment or adoption of carbon capture, use and storage solutions

- Decommissioning aged coal assets for re-purposing or repowering

Full or partial fuel conversion

From the fuel conversion perspective, one possibility will be to use natural gas to co-fire in the existing boilers. While major plant equipment such as boilers, steam turbines and heaters will be reused, modifications of boilers and burners are likely, with favorable long-term economics.

Factors that will influence the switch from coal to natural gas include stricter emissions standards; competitive natural gas prices; and newer and more efficient natural gas turbine technology.

When assessing fuel conversion possibilities, asset owners will need to consider the availability of uninterrupted and good quality alternative fuels, like natural gas, to support co-firing or full switch from coal to gas. With natural gas generation, investments to be considered will include building new liquefied natural gas (LNG) terminals, or using existing terminals that are close by or in-land gas pipelines. At the same time access to transmission and distribution networks must also be evaluated.

Key benefits of fuel conversion include infrastructure life extension, higher plant output, enhanced environmental performance, and improved operability and maintainability.

Retrofitting emissions control equipment

Another option is to add emissions control equipment to the existing coal-fired generation unit to reduce emissions. Asset owners will need to establish comprehensive compliance strategies and integrate environmental objectives into their business operations, considering regulatory drivers, operating conditions and plant configuration.

The aim will be to adopt technically proven environmental retrofit solutions that meet project financing requirements, have demonstrable emissions reductions and are able to return the assets to service as quickly as possible.

Options around carbon capture and utilisation, in some scenarios, may provide additional incentives in select regulatory environments or through the utilisation of captured carbon based on proximity of the power plant to potential offtakes requiring the resource as a raw material in their manufacturing processes.

Decommissioning aged coal assets for re-purposing or repowering

The third alternative is to decommission the coal assets. Decommissioning options for coal-fired plants include:

- Retiring and leaving in place

- Retiring and decommissioning the site for re-purpose

- Re-using for brownfield activities

- Re-purposing for renewable energy and energy storage

- Co-locating with data centers or utilities such as water treatment plants

- Converting to new fuel sources like gas or biomass

- Infinite lay-up or mothballing

A critical element of the decommissioning process is environmental permitting considerations and hazardous material dispensation.

One solution for repowering is to replace conventional coal boilers with simple cycle gas turbines and heat recovery boilers to reduce overall carbon emissions.

Key factors to consider for repowering are ease of integration, reuse of existing balance-of-plant equipment, operating flexibility, operations and maintenance costs, and technical risk mitigation.

Preparing for success

Selecting options that are cost-effective and capable of aligning with the current business model will be influenced by technical and financial factors such as fuel costs and price volatility; anticipated dispatch profiles; age and condition of plant equipment; capital costs, including gas pipeline; ongoing operation and maintenance costs, post-conversion; clean energy options, such as hydrogen and decarbonisation; and related supply chain implications such as mining concessions. Non-technical considerations will include environmental, local acceptance, political and future regulations.

Identifying the right decarbonisation path will require meticulous planning, market analysis, evaluations of multiple sustainable technology alternatives, cost economics and return on investment certainty within a tangible period. In mitigating project risks, socioeconomic and regulatory matters will need to be addressed early. Realistic evaluations of current assets for reuse will be invaluable to the decision-making process.

For successful coal retirement programs, key considerations for repurposing coal assets will need to be thoroughly understood. A priority will be to understand the criteria for selecting coal plants for repurposing. Other considerations will include investigating potential technology alternatives to uncover the best mix of technologies for each facility, managing offtake requirements, and minimising stakeholder impacts.

Equally important will be supportive government regulations and policies as they can help to accelerate the alternative use of coal plant sites, manage upstream supply chain transitions and facilitate access to funding necessary for repurposing coal power generation towards more sustainable low carbon power production.

Narsingh Chaudhary is Black & Veatch’s Executive Vice President & Managing Director, Asia Power Business. Harry Harji is Associate Vice President for Black & Veatch’s management consulting business in Asia.