The world is heating up, and Asia remains the fastest-warming region, with temperatures rising more rapidly than the global average. The continent is also the world’s most-disaster affected due to weather, climate and water-related hazards as of 2023.

To continue reading, subscribe to Eco‑Business.

Access all our exclusive content and archive — with a 7-day free trial. Then just US$5/month. Cancel anytime.

- Exclusive access to training across business and policy topics

- Direct access to industry leaders at Eco-Business events

- A seat among the decision makers shaping the region's sustainable development

“The increase in the occurrence and severity of disasters due to climate change not only inflicts immense human suffering and damages ecosystems, but also hinders economic stability and development,” said Francesco Ricciardi, senior environmental specialist at the Asian Development Bank (ADB).

Last year, economic losses from natural disasters reached US$65 billion in Asia. Yet only 9 per cent of those losses were covered by insurance. By 2025, Asia alone is predicted to account for US$0.93 trillion of uninsured risks – the global protection gap in 2010.

The global protection gap has been trending upwards since 2010. By 2025, Asia and the Pacific is expected to account for nearly half of the total, reaching US$0.93 trillion, the same amount as the protection gap for the world in 2010. Image: PwC Bermuda

Traditionally, funds from donor countries and international organisations played a significant role in post-disaster relief capital. However, political and administrative factors often delay capital transfer and hinder response efforts.

Parametric insurance offers a quicker alternative. Payouts are automatic, enabling timely rehabilitation and minimising long-term socio-economic impacts, said Ricciardi.

In regions of Asia where development funds are limited and foreign aid unreliable, parametric insurance could fill a critical gap by reducing uninsured risks.

What is parametric insurance?

Parametric insurance relies on a set of predefined parameters, or event triggers. When these parameters are met or exceeded, the insurance cover is triggered, and a payout is made automatically, regardless of actual physical losses sustained.

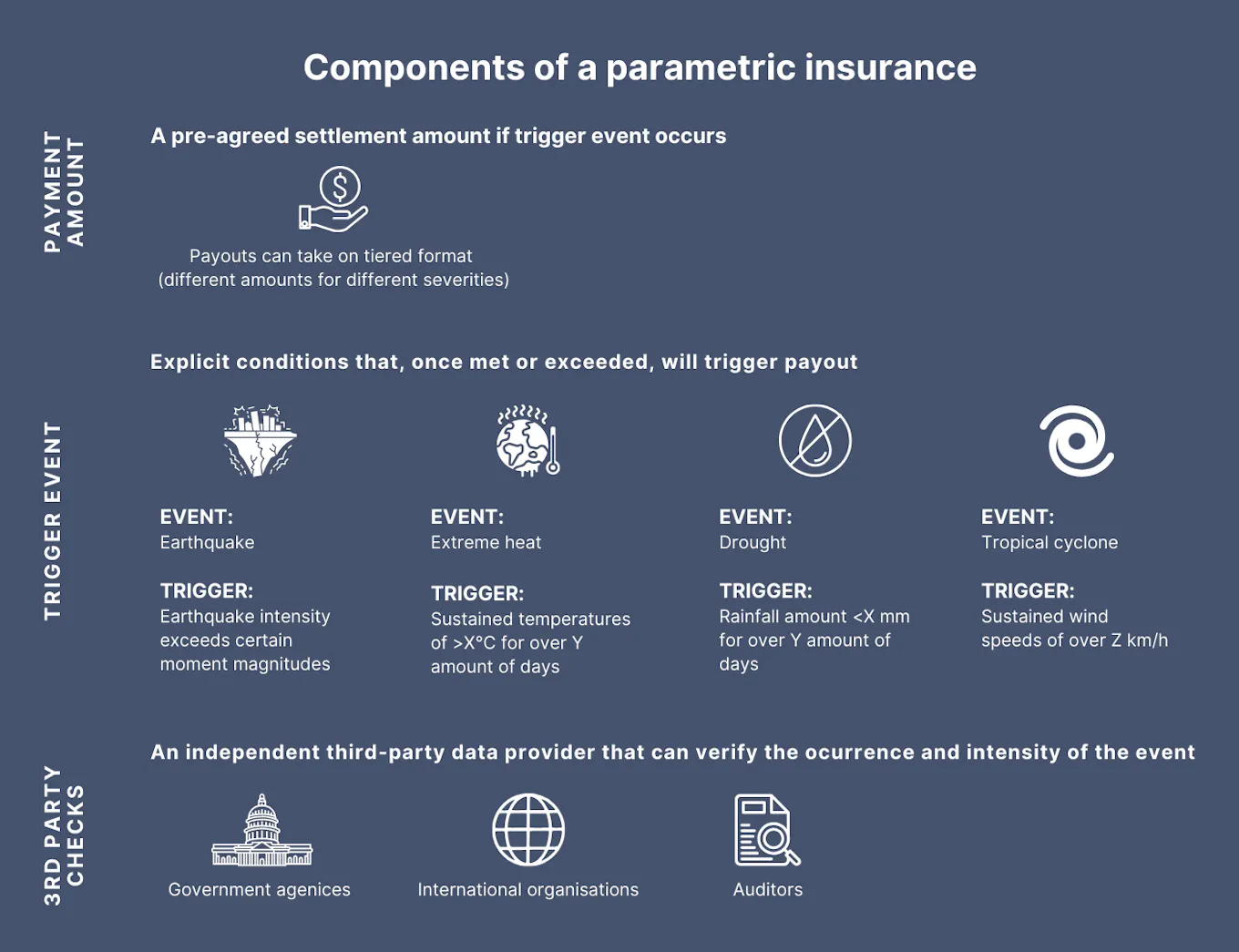

A parametric insurance policy has three key components: a pre-agreed payment amount, a predefined trigger event, and third-party checks to verify event occurrence.

Image: Eco-Business

How does parametric insurance differ from traditional insurance?

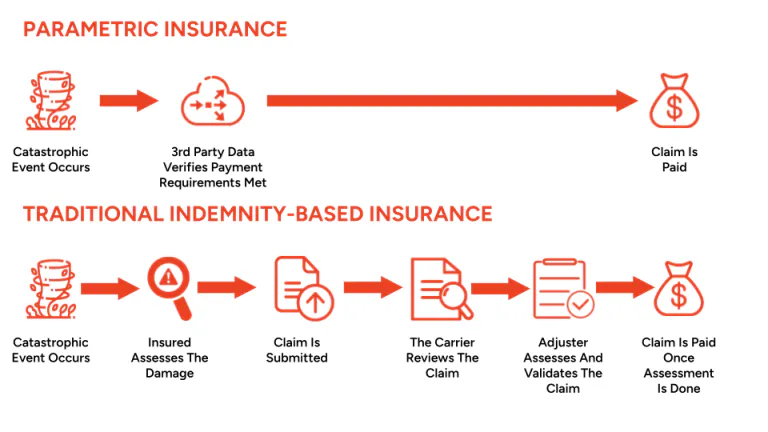

Traditional insurance is indemnity-based, which means claims are paid only after damages have been assessed and verified, and settlement can take months to years.

Comparatively, little administration and minimal proof of actual losses are required for parametric insurance. An independent third party only needs to verify that the terms for payment have been met. The streamlined claims process allows much faster payouts, with the funds being disbursed within a month.

Parametric insurance offers a more streamlined process as compared to traditional indemnity-based insurance. This allows payouts to reach affected communities much faster, which aids crucial recovery efforts. Image: Risk and Insurance Education Alliance

Parametric insurance is typically designed to complement, rather than replace, traditional insurance products. It aims to reduce risk exposure by covering areas not insured by conventional products.

“Policyholders can seek the best of both worlds with a hybrid structure that combines parametric and conventional insurance. This allows for a fast payment following the insured event for immediate recovery, whilst the full amount of damage can be assessed subsequently,” said Christopher Au, director for global brokerage WTW’s Asia-Pacific Climate Risk Centre.

Why is parametric insurance increasingly attractive in Asia?

The elimination of the claims verification and adjustment process allows funds to reach policyholders much faster. This significantly reduces the financial burden of post-event response, which is crucial for disaster-prone Asia.

For instance, when super Typhoon Rai – known locally as Typhoon Odette – struck the Philippines in 2021, a power utility company in Cebu was paid within just 12 days after the event by global insurance firm Swiss Re, under a parametric insurance product.

According to the policy’s terms, reported to be a “cat-in-a-box” type structure, the payout was triggered when the storm’s sustained wind speeds exceeded predefined levels while passing through the region. These funds could then be used for restoration efforts, minimising disruptions to an essential service.

“Cat-in-a-box”

“Cat-in-a-box” is the most popular form of parametric insurance structure, due to its simplicity of comprehension and execution.

“Cat” refers to the catastrophe the policyholder is being insured against, such as typhoons or earthquakes. The box demarcates a specific, predefined area which the insurance will cover, although it can take any shape.

If the catastrophe meets both the pre-agreed parameter threshold and occurs within the box, a payout will be triggered.

Rapid liquidity for post-disaster response is increasingly pertinent for Asia, which has borne the brunt of climate catastrophes. The region is now 25 times more likely to be affected by natural disasters than Europe, according to the ADB.

“The continued increase in losses from natural catastrophes and the increase in prices for conventional insurance has resulted in a tightening of general terms and conditions, and companies across Asia have to think more carefully about their existing risk transfer arrangements,” said Au.

Parametric insurance also offers coverage for risks not insured by traditional market products.

For instance, Sri Lanka’s coastal shrimp farms have been insured against four weather risks – earthquakes, typhoons, excessive rainfall, and heat stress – under Asia’s first four-peril parametric insurance product launched by WTW.

These weather events are not covered by existing insurance products, although weather risks pose the most common threats to shrimp farming.

The product was designed for Taprobane Seafood Group, the country’s leading seafood company. It is expected to aid Taprobane’s development of sustainable shrimp farming, which will provide local employment opportunities, while supporting aquaculture growth and easing food security concerns.

Downsides to parametric insurance?

While divorcing actual losses from claims settlements expedites payouts, this mechanism also results in basis risk – the difference between the actual financial impacts suffered by the insured party, and the payout received under the insurance policy.

Recovery efforts could also be undermined if the payout is insufficient to cover losses. In the worst cases, insured parties could suffer losses without parameters even being triggered.

This was the case for Malawi’s 2016 drought, where no payouts were triggered despite some 6.5 million people assessed as needing assistance. The insurer had used a faulty model which severely underestimated the number of individuals affected by the drought.

Following a reassessment, US$8 million was finally paid out to Malawi’s government in January 2017, more than half a year after requests were filed. However, the amount was deemed to be “too little, too late”, as the government was forced to use other means to cover economic losses estimated at US$395 million.

Since parametric insurance is a relatively new development, the lack of regulatory and governance frameworks has also hindered adoption.

In jurisdictions without separate policies for parametric insurance, policies are subject to the same indemnity laws as traditional insurance, slowing down payment.

However, key developments such as regulatory sandboxes and centralised platforms for product offers are expected to streamline the process in Asia.

“There is always inertia and concern when trying something new. Comfort and track record with the reliability of the product and approach is important, and this is improving over time,” said Au.

The parametric insurance landscape in Asia

Presently, China dominates the region’s parametric insurance market and is expected to remain so until 2028, reaching a market value of US$1.6 billion.

Several initiatives, such as the Southeast Asia Disaster Risk Insurance Facility (SEADRIF), have also been developed to safeguard the region against climate-driven hazards. SEADRIF is the first regional catastrophe risk insurance. For instance, it provided coverage against flood risks in Laos in August 2023, with two payouts totalling US$1.5 million for flood relief efforts.

There are also smaller scale microinsurance projects for individual stakeholders. Often, these target smallhold farrmers who may not possess extensive funds, but still have assets to insure.

In India, a microinsurance project for climate change and disaster resilience has been implemented to extend climate change risk coverage to low-income households in rural areas. Supported by the ADB, the fund has disbursed US$59.5 million as of March this year.

Separately, investments have been made into infrastructure such as satellites to capture data on the causes and impacts of natural catastrophes. In Southeast Asia, these developments have helped build up a knowledge profile of the region, enabling more accurate insurance formulation to reduce basis risk.

“Improvements in data analytics, remote sensing technology, and climate modelling will increase the precision of parametric triggers, making insurance products more customised and effective,” said Ricciardi.

A sustainable solution to guard against climate risks?

Parametric insurance will not be the panacea for protection against climate-related disasters. Experts have warned that with climate change causing more damage than projected, and too little money being spent on protecting populations, such insurance projects could struggle in the long run.

For example, Kenya’s Livestock Insurance Programme paid out 1.2 billion Kenyan shillings (US$8.8 million) for drought damages between 2015 and 2021, but only collected 1.1 billion Kenyan shillings (US$8.1 million) in premiums. The scheme has since been replaced.

“Parametric insurance offers a temporary solution by providing immediate funds post-disaster, ensuring that communities can bounce back quickly while longer-term adaptation measures are carried out,” said Ricciardi.

A wider view on risk also helps the company to assess the total cost of risk, so that increased investments in adaptation and resilience can also be understood as reducing the need for risk transfer, added WTW’s Au.