One bright spot in the unprecedented stock market volatility brought on by the Covid-19 pandemic is that most US environmental, social and governance (ESG) index funds are outperforming traditional index funds.

Index funds are designed to track specific indexes, like the Dow Jones or S&P 500. They are among the most popular investments by investors, including retirement savers. ESG index funds incorporate data points relating to a company’s ESG profile as well as traditional financial metrics to screen and weight securities.

Most ESG funds now in existence were launched in 2013-2014, when the approach gained momentum. The Covid-19 market crash, the worst single-day drop since 1987, is the first major test of these funds’ resilience.

This test is unfolding just as new regulations aim to limit investment in ESG funds. In June, the US Department of Labor proposed amendments to make it more difficult for retirement plans regulated under the Employee Retirement Income Security Act (ERISA), including 401ks, to include ESG funds.

The Labor Department suggested that ESG investing may prioritise environmental or social causes over a financial return, the top priority of retirement plans.

Ironically, the Labor Department’s proposed rule was published at a time when most ESG index funds have outperformed conventional funds. Twenty-four of 26 ESG index funds covering both US and global stocks outperformed the comparable conventional funds.

Why are ESG funds outperforming S&P500 during the coronavirus market crash?

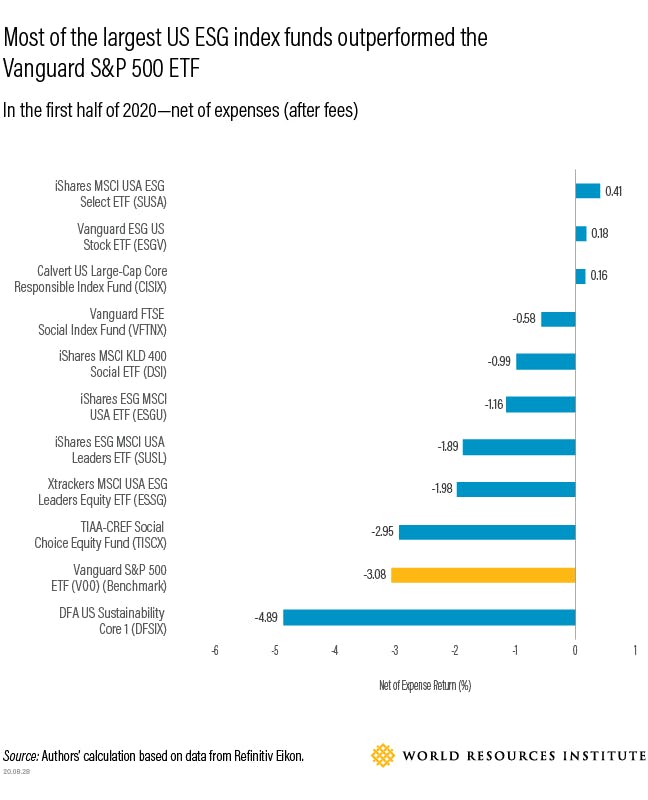

We analysed the 10 largest US open-ended ESG index mutual funds and exchange-traded funds (ETFs) because ESG index funds are usually cheaper than actively-managed ESG funds and are more likely to be included in retirement plans.

All of them belong to the same Morningstar fund category, US Large Blend, so their returns are often similar to those of the S&P 500 Index. Accordingly, we used the Vanguard S&P 500 ETF (ticker: VOO), a highly-rated US Large Blend ETF that tracks the S&P 500 Index – with the lowest expense and tracking error among peers – as our benchmark.

When creating a fund, fund managers must choose how to allocate their assets among the sectors of the economy. They must also choose which companies will represent those sectors, and how to distribute the allocation to a sector between the companies representing that sector. But which of these choices drove ESG index funds’ recent success?

We used the popular, simple Brinson–Fachler (BF) model to determine the source of the return difference between ESG index funds and the benchmark – sector allocation, stock selection, or a mix. (While the BF model is often used to analyse actively-managed funds, ESG index funds can be considered quasi-active because they use additional rules to select and weigh stocks differently than a pure market-cap weighted index fund.)

Here’s what we learned:

1. Nine of the 10 largest US ESG index funds outperformed the S&P 500 in the first half of 2020

The ESG funds in our analysis outperformed VOO by an average of 2.1 percentage points, net of expenses (that is, after fees). To put this in more concrete terms, an investor who divided $1 million evenly among the top 10 ESG index funds instead of VOO in January 2020 would have had $17,000 more in June.

ESG funds outperformed S&P 500 benchmark. Image: World Resources Institute

2. ESG index funds benefited from their tendency to invest less in energy and more in IT

The allocation effect determined by the BF model refers to the difference in returns caused by the fund having different sector weights than the benchmark. In the case of these ESG funds’ outperformance, sector allocation contributed an average of 0.77 percentage points, most of which came from how they approached the energy and information technology (IT) sectors – avoiding the former and investing more heavily than VOO in the latter.

Others have also attributed the outperformance of ESG funds in 2020 to their lower exposure to the year’s worst-performing sector, energy, and higher exposure to the best-performing sector, IT. These ESG index funds’ average energy exposure was 1.33 percentage points less than VOO, and their average IT exposure was 1.71 percentage points more than VOO.

The ESG index funds with clear strategies for excluding or underweighting companies involved in fossil fuel (VFTNX, DFSIX, CISIX and ESGV) tend to have the lowest exposure to energy stocks and generally higher exposure to IT stocks.

3. Most ESG index funds also benefited from stock selection within each sector

Within the BF model, selection effect refers to the value added (or lost) by the fund investing more or less in particular individual stocks within the sector compared to the benchmark. Stock selection contributed an average of 0.65 percentage points for these ten ESG index funds. In other words, ESG index funds not only benefited from avoiding energy and investing in IT stocks – they also did better by picking good stocks within sectors, too.

DFSIX is an outlier as it performed worse than VOO and its peer ESG funds. This could be because it had the greatest exposure to smaller companies, which are more vulnerable to the coronavirus pandemic than larger ones. However, some other funds (TISCX and ESGV) also have exposure to small stocks and did well. DFSIX’s underperformance would require future investigation beyond the scope of this blog post.

Although most ESG index funds had positive selection effects on average, they varied greatly across sectors. The average positive stock selection effects were highest in financials, health care and industrials, while the average negative stock selection effects were highest in energy and consumer discretionary sectors. This could be due to factors beyond the funds themselves, as most funds track ESG indexes provided by third-party index sponsors.

Fund prospectuses and index methodologies only reveal so much about the investing approach and index construction, though. To varying degrees, fund approaches and indexes remain a “black box,” limiting our ability to understand how they were successful (or unsuccessful) at selecting stocks within each sector.

In addition, fund managers, index providers and investors have significant differences in defining and interpreting ESG criteria, which could arrive at inconsistent assessment of the same company. Investors would stand to benefit from greater transparency about investing approaches and methodologies from the funds and indexes.

The current stress test for these funds is ongoing and there is great uncertainty about the future. We will need to see whether our initial findings hold over longer periods, but so far, it appears that ESG index funds are positioned to continually weather volatility better than their non-ESG counterparts.

ESG index investing could help investors meet financial objectives and achieve retirement goals

Although our analysis covered a short period of time, the consistent outperformance of most large ESG index funds from both sector allocation and stock selection during the Covid-19 pandemic illustrates that ESG index investing does not necessarily harm returns. In fact, ESG index funds may help investors manage downside risk better than traditional index funds.

This recent outperformance only adds to existing evidence in favor of ESG investment strategies. In light of this, the proposed rule by the Labor Department to increase the administrative, financial and legal burden to include ESG funds in retirement plans could hurt retirement investors by limiting their access to important and potentially better investment options.

Lihuan Zhou is Associate II of World Resources Institute’s Sustainable Finance Centre. Yilu Wu is Research Analyst II of World Resources Institute’s Sustainable Finance Centre. Joseph Heavner is a Sustainable Investing Intern at World Resources Institute’s Sustainable Finance Centre. This post is republished from the WRI blog.